When building an investment portfolio, one of the first decisions investors face is whether to keep things extremely simple with a single ETF or create a slightly more diversified portfolio using multiple ETFs. Both approaches can be highly effective, and both have loyal supporters among long-term investors.

The debate between a one-ETF portfolio and a three-ETF portfolio is not necessarily about right versus wrong. Instead, it comes down to balancing simplicity, diversification, control, and flexibility. While both strategies can help investors build wealth over time, understanding their differences can help determine which approach best fits your goals.

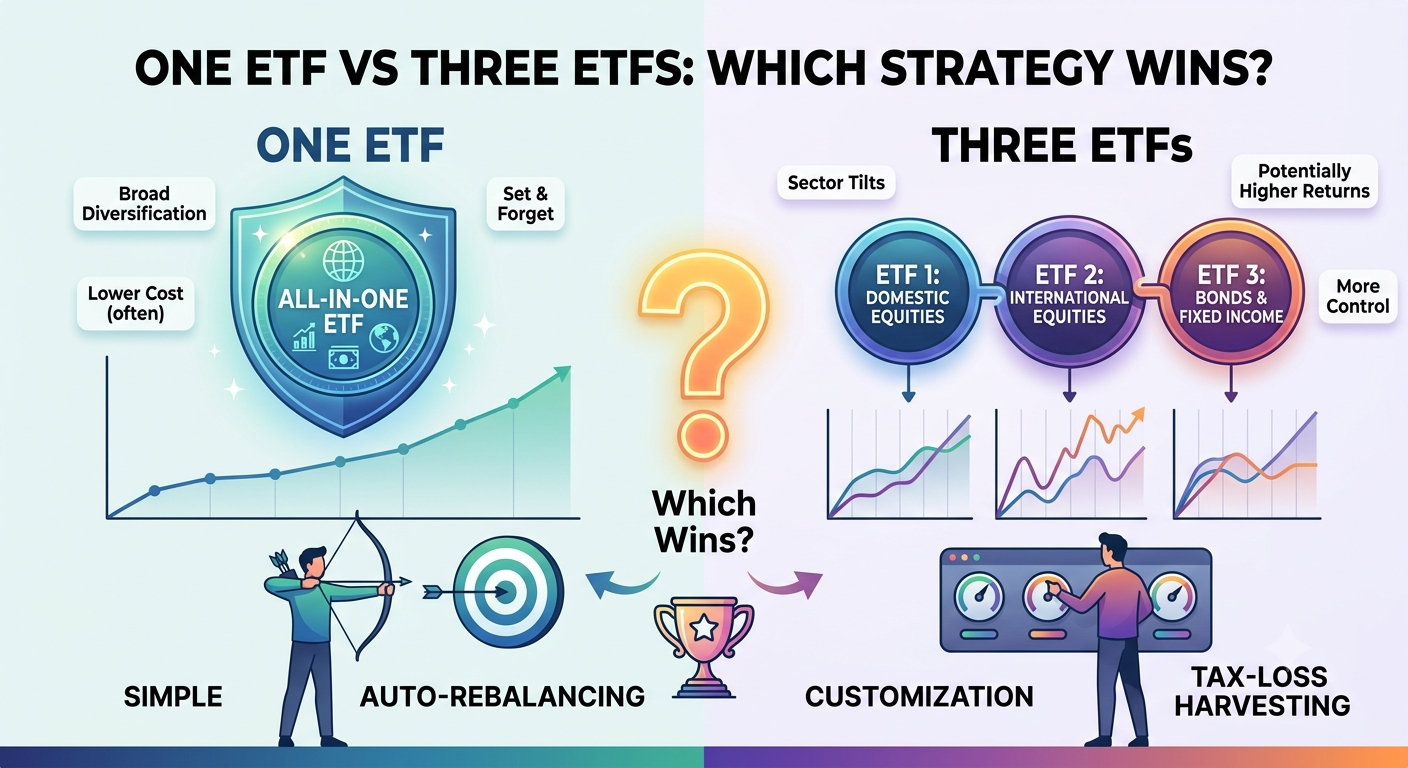

The One-ETF Strategy

A one-ETF portfolio is exactly what it sounds like: investing all your money in a single broadly diversified fund.

One of the most popular examples is the Vanguard Total World Stock ETF (VT). This ETF holds thousands of companies from both developed and emerging markets around the world.

By owning one fund, investors gain exposure to:

- U.S. stocks

- International stocks

- Large-cap companies

- Mid-cap companies

- Small-cap companies

- Developed markets

- Emerging markets

In many ways, VT represents a complete global stock portfolio in a single investment.

Advantages of a One-ETF Portfolio

The biggest benefit is simplicity.

Investors only need to:

- Buy one fund

- Monitor one position

- Reinvest dividends

- Make regular contributions

There is no need to decide how much to allocate between U.S. and international stocks or when to rebalance. The ETF provider handles those decisions automatically.

This simplicity can also reduce behavioral mistakes. Investors are less likely to tinker with their portfolios when there is only one fund to manage.

Drawbacks of a One-ETF Portfolio

The primary disadvantage is lack of customization.

For example, investors cannot easily:

- Increase U.S. exposure

- Reduce international exposure

- Add bonds separately

- Adjust allocations based on age or risk tolerance

The portfolio is essentially locked into the ETF’s underlying structure.

For some investors, this is a benefit. For others, it may feel restrictive.

The Three-ETF Strategy

The classic three-ETF portfolio is designed to provide broad diversification while maintaining flexibility.

A common version includes:

- Vanguard Total Stock Market ETF (VTI)

- Vanguard Total International Stock ETF (VXUS)

- Vanguard Total Bond Market ETF (BND)

Instead of relying on a single fund, investors control the allocation of each asset class.

A typical allocation might be:

- 60% VTI

- 30% VXUS

- 10% BND

However, investors can modify these percentages to match their own objectives.

Advantages of a Three-ETF Portfolio

The biggest advantage is flexibility.

Investors can:

- Increase stock exposure when young

- Add more bonds as retirement approaches

- Adjust international allocation

- Customize risk levels

- Rebalance according to personal preferences

This approach provides greater control over portfolio construction.

Many investors appreciate being able to tailor allocations rather than accepting a fixed structure.

Drawbacks of a Three-ETF Portfolio

The trade-off is complexity.

Although three ETFs are still relatively simple, investors must:

- Monitor multiple holdings

- Decide on allocation percentages

- Rebalance periodically

- Make asset allocation decisions

While these tasks are not difficult, they require more involvement than a one-fund portfolio.

Comparing Diversification

Surprisingly, both approaches can offer excellent diversification.

A one-fund solution like VT already holds thousands of global stocks.

A three-fund portfolio also provides broad diversification but adds exposure to bonds and allows investors to choose their preferred stock allocation.

In terms of stock diversification alone, the difference is relatively small.

The bigger distinction is whether bonds are included and how much control investors want over asset allocation.

Comparing Returns

Historically, returns depend more on asset allocation than the number of ETFs owned.

For example:

A one-ETF portfolio invested entirely in global stocks may outperform a three-fund portfolio during strong stock market periods because it maintains a higher equity allocation.

However, a three-fund portfolio containing bonds may experience smaller losses during market downturns.

The winner often depends on:

- Market conditions

- Investment horizon

- Risk tolerance

- Allocation choices

There is no guarantee that one approach will consistently outperform the other.

Comparing Risk

A one-ETF portfolio invested entirely in stocks generally carries more risk than a three-fund portfolio that includes bonds.

During bear markets, stock-only portfolios can experience significant declines.

A bond allocation can help reduce volatility and provide stability during periods of market stress.

Investors must decide whether they value maximum growth potential or smoother portfolio performance.

Which Strategy Is Better for Beginners?

For complete beginners, a one-ETF portfolio can be an excellent starting point.

The simplicity removes many common obstacles:

- No allocation decisions

- No rebalancing

- No complicated portfolio management

A fund such as VT allows investors to focus on saving and investing consistently rather than worrying about portfolio construction.

As knowledge and experience grow, some investors eventually transition to a three-ETF portfolio for greater flexibility.

Which Strategy Is Better for Long-Term Investors?

Many long-term investors prefer the three-ETF approach because it offers greater control over risk management.

As retirement approaches, adding bonds often becomes more important. A three-fund portfolio allows investors to gradually shift allocations without changing their overall strategy.

The ability to customize asset allocation is one of the main reasons the three-ETF portfolio remains a favorite among experienced index investors.

The Real Winner: Consistency

The truth is that neither strategy wins solely because it uses one ETF or three ETFs.

The biggest determinant of success is investor behavior.

A simple portfolio that you consistently contribute to for 20 or 30 years will likely outperform a more sophisticated portfolio that you constantly modify, trade, or abandon during market downturns.

Successful investing is often less about finding the perfect allocation and more about maintaining discipline through changing market conditions.

Final Thoughts

The choice between a one-ETF portfolio and a three-ETF portfolio ultimately comes down to simplicity versus control.

A one-fund solution such as the Vanguard Total World Stock ETF (VT) offers maximum convenience and global diversification in a single investment. It is ideal for investors who want a truly hands-off approach.

A three-fund portfolio built with Vanguard Total Stock Market ETF (VTI), Vanguard Total International Stock ETF (VXUS), and Vanguard Total Bond Market ETF (BND) provides greater flexibility and risk management options, making it attractive for investors who want more control over their asset allocation.

In the end, the strategy that wins is the one you can follow consistently, keep invested through market volatility, and maintain for decades. Simplicity and discipline will almost always matter more than the number of ETFs in your portfolio.